Overview

Equities meandered for the first part of the month of September but finished decidedly up, courtesy of a .50% interest rate cut by the Federal Reserve (FED).

The S&P 500 rose 2.14% overall while the Nasdaq composite gained 2.76%. The Russell 2000 (Small Cap Stocks) increased by a mere .70%., continuing to lag larger capitalization indices.

In international markets, the EPAC BM Index of developed economies (ex-US) rose .58% while the MSCI EM (emerging markets) progressed a whopping 6.45%. A declining USD coupled to a reduction in US interest rates contributed to the outsized performances of emerging equities. Most emerging nations are indebted in USD and a reduction of both the value of the USD and the level of interest rates constitutes a double win.

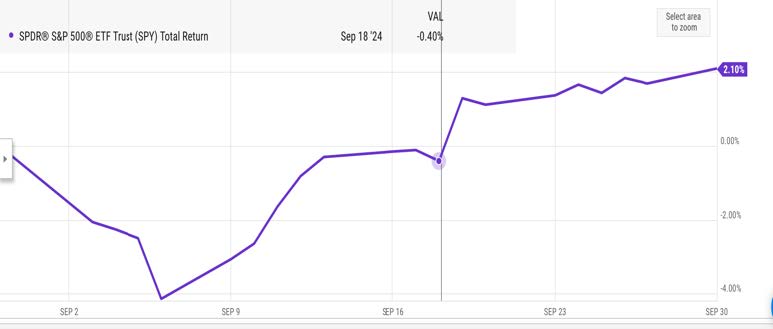

The graph below illustrates the initial equity decline and subsequent recovery of US equities, post FED’s decision (vertical line):

In September, US fixed income markets performances were positive. The AGG index finished the month up 1.34%, while Investment Grade and High Yield bonds rose respectively 1.77% and 1.62%. The Bloomberg municipal index was up .99%.

Our median portfolio gained 1.67% in September. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 1.77%. YTD our median portfolio, net of fees, is up 10.84% vs 11.50% for our reference index.

Market developments

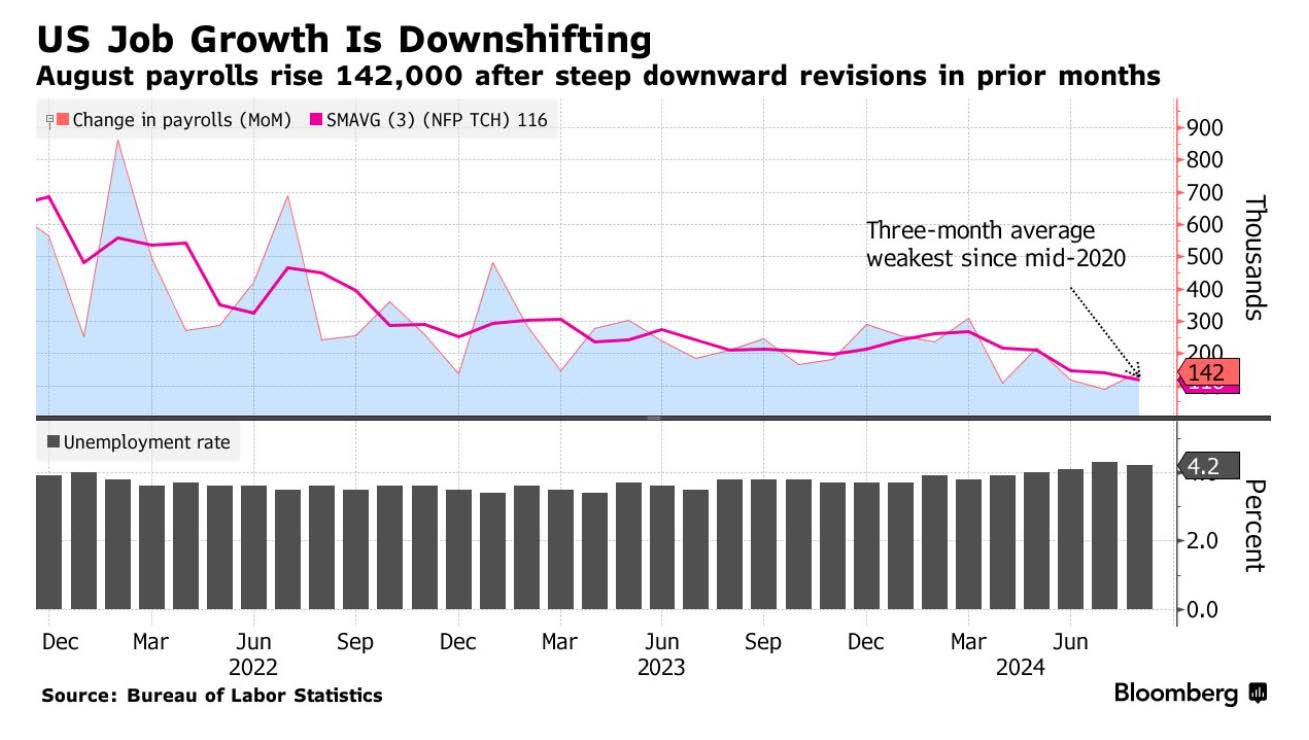

The month of September started with economic data pointing to a slowdown in activity that contributed to a relatively somber tone for equities. As shown in the graph below, employment numbers for the month of August confirmed the downward trend of the previous quarter.

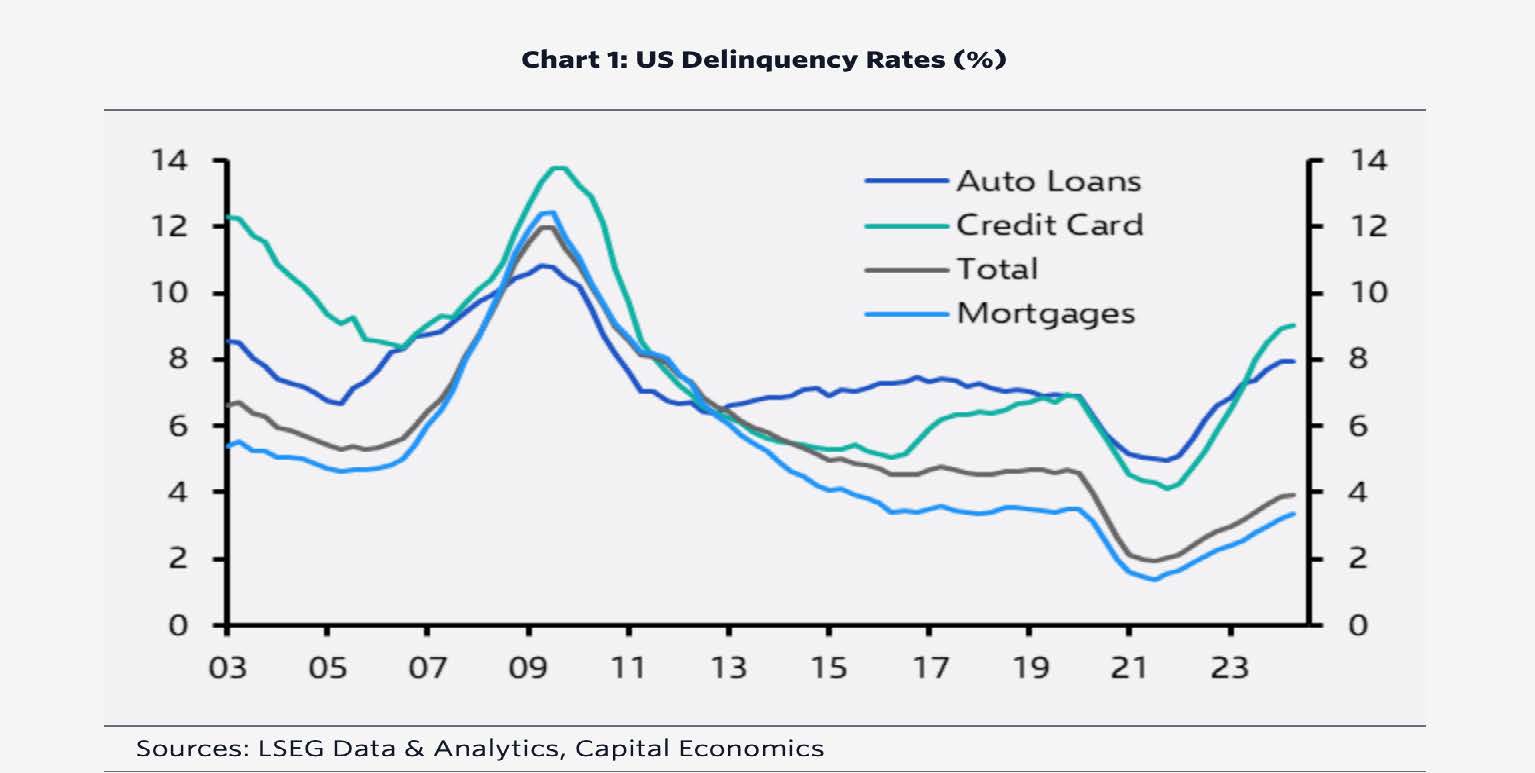

In addition, other signs of financial stress, as illustrated in the delinquency data below, added to investors’ concerns about an impending recession.

In the aggregate, these signs finished to convince the FED that the risk to the US economy had shifted from inflationary threats to recessionary threats.

In response to these threats, in a quasi-unanimous decision on October 17, the FED announced a reduction of the federal funds rate of .50%. This reduction stood at the higher end of the .25%-.50% range anticipated by market participants and propelled equities up by about 2.5% to finish the month on a positive note.

Portfolio Commentary

Investors appear to be gradually coming to the realization that the FED may have succeeded in taming inflation without pushing the US economy into a recession. The positive reaction to their .50% rate reduction is a good sign that investors believe that the economy is slowing but is not going to drop off a cliff.

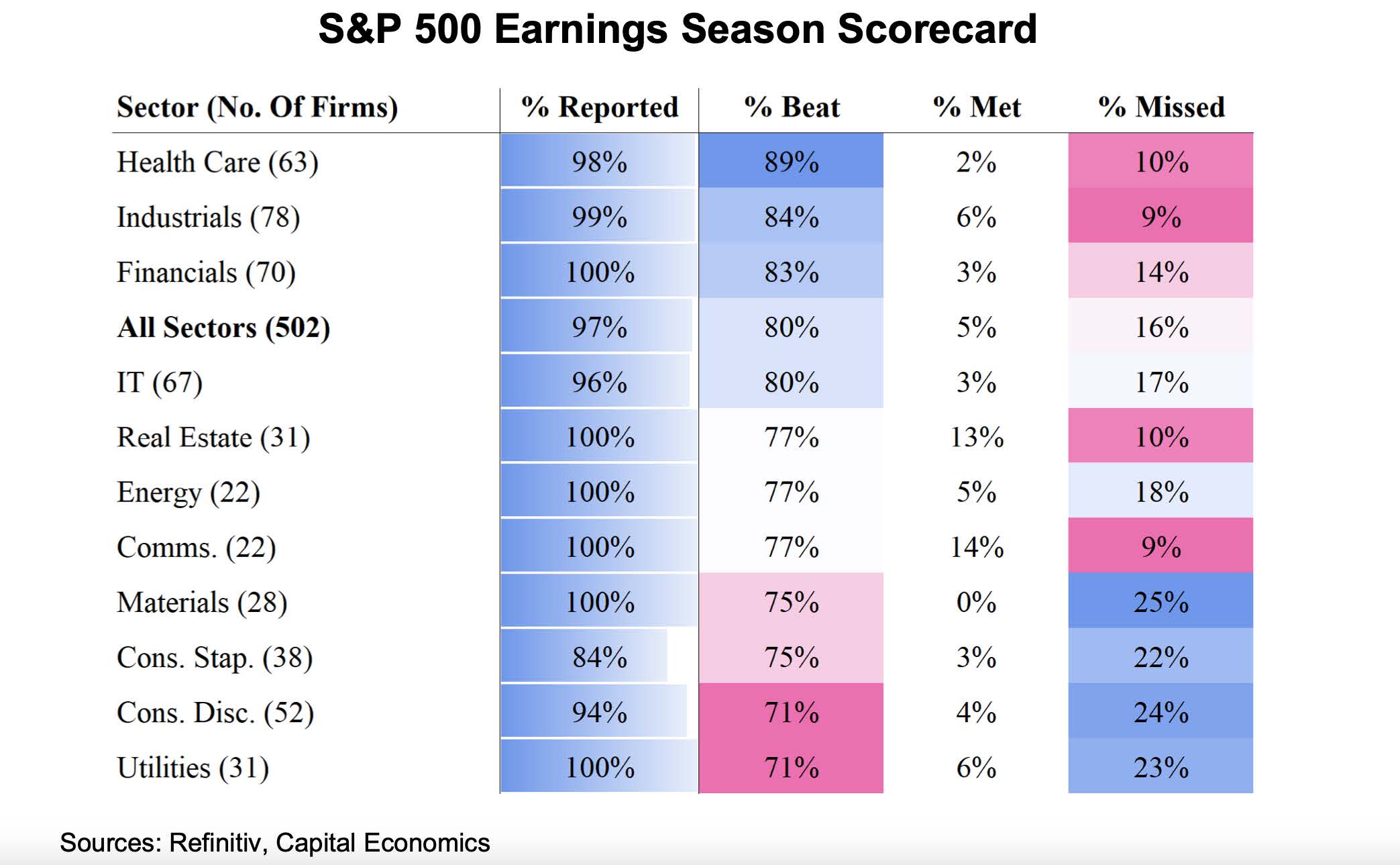

That feeling is reinforced by the relatively good third quarter earnings numbers released by corporations since mid-July, as shown below:

In the end, third quarter corporate earnings ended up 13% overall compared to last year (for S&Ps’ 500 corporations). A supportive result.

In that context, I did not alter our current equity allocations. My investment actions were limited to increasing the duration of our fixed income holdings (duration is a measure of interest rate sensitivity). I did so by buying AGG with the proceeds of maturing US Treasury bills.

Additionally, I continued to substitute RSP, the equal-weighting S&Ps’ 500 ETF, for SPY, its traditional capitalization-weighted brethren.

At this juncture, with the US presidential election closing in and wars in the middle east and in eastern Europe, I remain ready to abruptly reduce our exposure should the situation further deteriorate.

Conclusion

Currently, my biggest worries come from the international situation and the role US elections play in that narrative.

It is improbable that the middle east conflict will simmer down until the US elections have passed. The Administration will not take a decisive step until then and players on both sides of the conflict know it. As a result, an intensification of the conflict over the four coming weeks is more likely than not. The same applies to the Ukrainian situation. Putin will pound Ukraine even harder as the Administration imposes a “no-action” agenda on itself.

The immediate consequences of this situation are: 1) A rising USD, 2) Rising oil prices; both of which directly affect international equities. This sector is likely to continue to slide downward. It has done so over the past few days. I do not yet see a catalyst for a respite.

US equities should hold better, but with valuations already historically high a correction is not implausible, particularly if the incoming economic data show signs that the economy is softening more than previously anticipated.

This morning’s good unemployment numbers for September offer reasons to remain optimistic though.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980