Overview

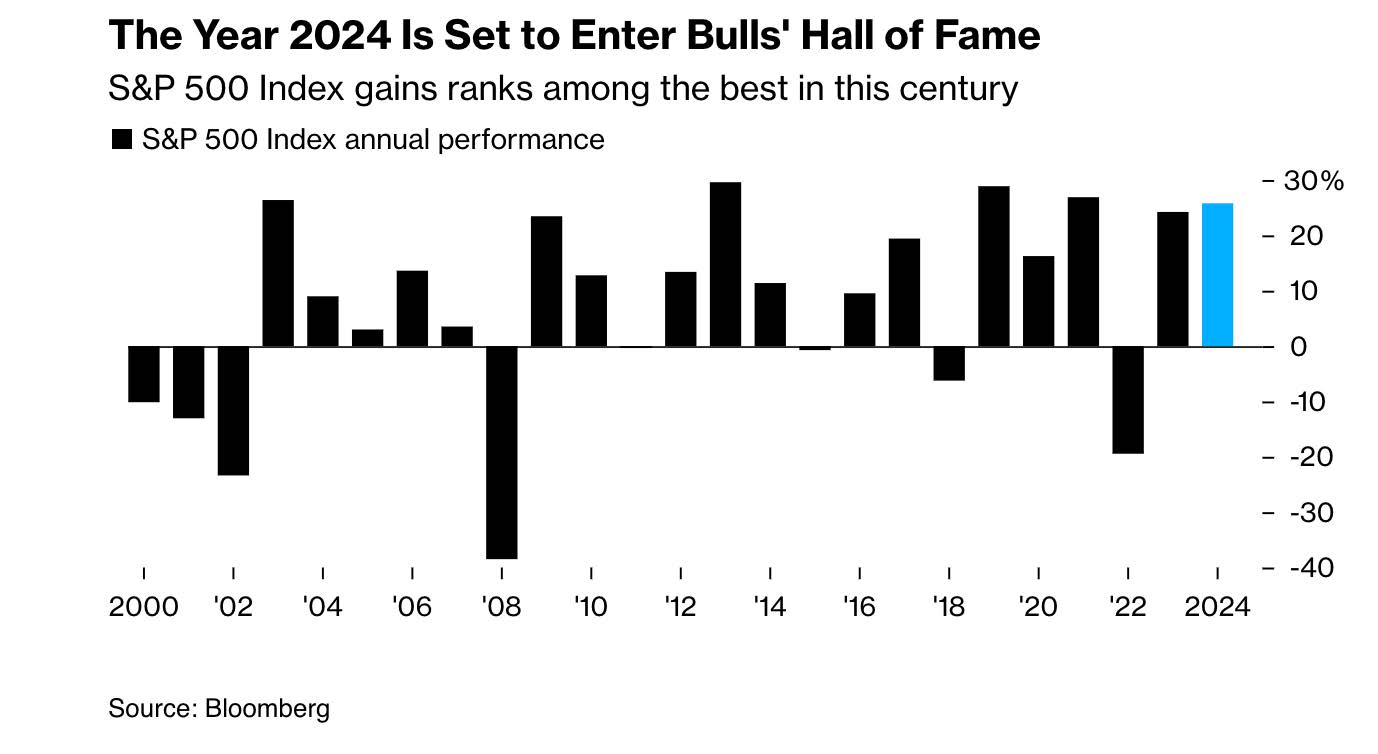

In November, Trump’s victory, the continuation of supporting US economic data, and a Federal Reserve Bank (Fed) set on further pushing interest rates down all contributed to spectacular equity performances in the US.

The S&P 500 rose 5.87% overall, while the Nasdaq composite jumped 6.29%. The Russell 2000 (Small Cap Stocks) responded to Trump’s electoral victory with a compelling and unusual 10.97% performance.

The situation was quite different elsewhere.

The EPAC BM Index of developed economies (ex-US) remained flat, while the MSCI EM (emerging markets) dropped 3.66%. A sharply rising USD, coupled with the threat of tariffs likely to be imposed by the incoming US Administration, contributed to the sorry performance of non-US equity markets.

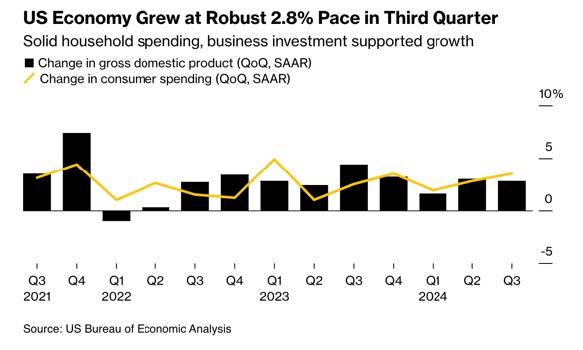

In a generally weakening global economic environment, the graph below provides an illustration of the continuing good health of the US economy; some would say of its exceptionalism:

In November, US fixed income markets performances were up, supported by the Fed’s interest rate easing stance.

The AGG index finished the month with a 1.06% gain, while Investment-Grade and High-Yield bonds rose respectively 1.34% and 1.15%. The Bloomberg municipal index was up 1.73%.

Our median portfolio was up 3.80% in November. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 2.57%. YTD our median portfolio, net of fees, is up 13.58% vs 11.86% for our reference index.

Market developments

Trumps’ electoral victory, assisted by supportive economic news, explains in good part the amazing performance of US equity markets in November.

The new administration intends to prolong the 2017 tax cuts offered to the corporate sector. They are set to expire in 2025. Additionally, it is expected to deregulate, or loosen regulations, in various sectors of the US economy. In combination, these two policies will contribute to supporting corporate profits, the main engine of the stock market. Hence the market reaction in November.

The new administration is also expected to implement protectionist policies that the markets perceive as being broadly favorable to US based companies with little exposure to the outside world. This explains the spectacular performance of the Small Cap sector this past month. That said, tariffs are also expected to exact a cost on the US economy in the form of higher prices. This will likely temper the FED’s easing stance going forward.

With this as a backdrop and with little talk of fiscal discipline from the new administration, bond markets have started putting a bottom on how far interest rates will go down. As a matter of fact, the long end of the yield curve has steepened (longer term rates are higher at the end of this month compared to where they were before the elections). In combination, these factors make me question whether the current rally will be sustained beyond February, once the potential downside of these policies is easier to perceive.

For now, the US economy remains on a relatively strong footing and the recent performance of US equities reflects it, as shown below

Portfolio Commentary

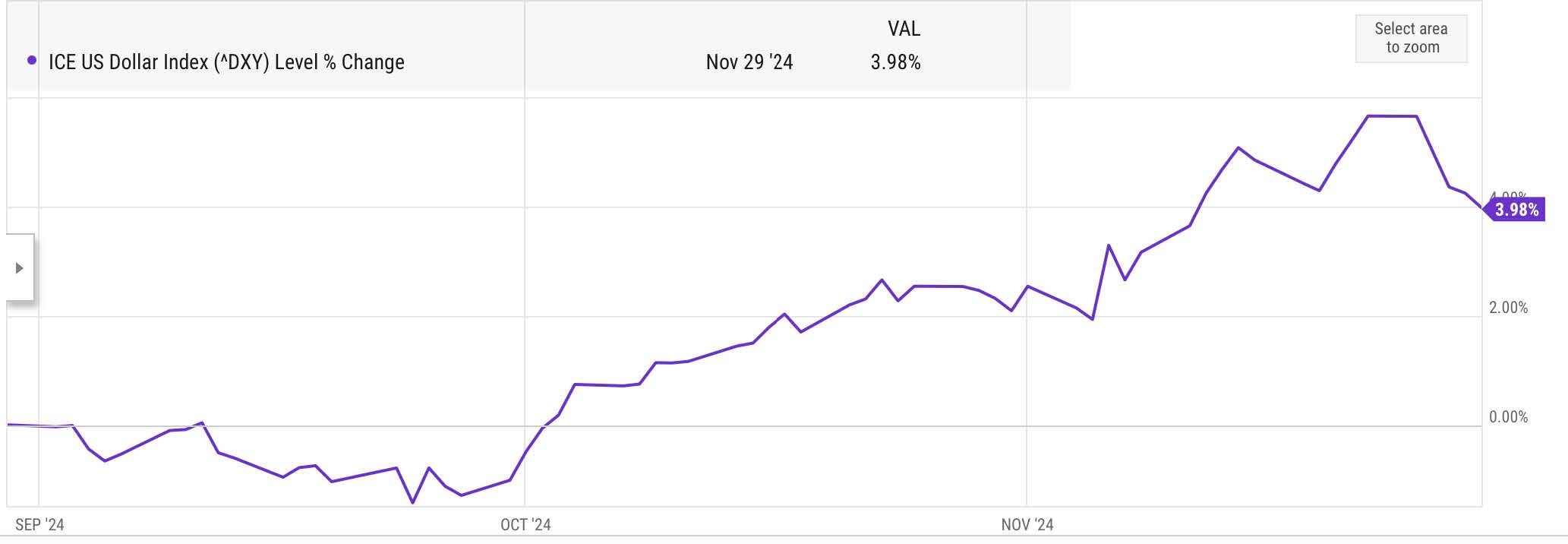

In November, with our international exposure reduced to our investment in Air Liquide, we managed to escape most of the damage caused to international equities by a rising USD.

Over the past three months, the USD has risen by close to 4% against a basket of other major currencies, as shown in the graph below:

This has made it that much more difficult for any equity market outside of the USA to perform.

Meanwhile, in the US, Trump’s return to the presidency has been particularly favorable to those market sectors that had been trailing. The financial sector has been one such beneficiary and our SCHW holdings moved up 17% in November. This caused me to sell about two-thirds of our investment. I am glad to report that our overall return on this investment since March 2023 has matched or surpassed that of the S&P 500. After enduring sharp ups and downs, I am happy with our overall result. That investment returned about 55% since we first made it in March 2023.

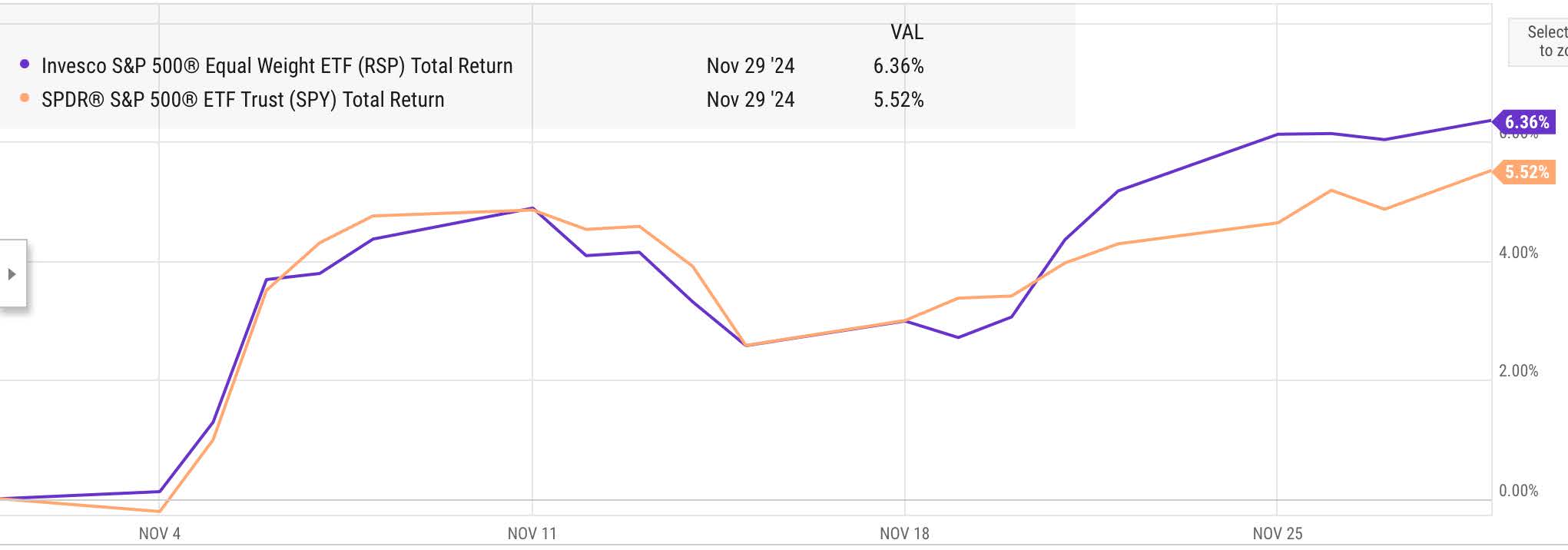

This same market trend, favorable to sectors outside of technology, explains the relative recent outperformance of RSP, the equal-weighted S&P 500 EFT, vs. that of SPY, its capitalization-weighted counterpart. As shown on the graph below:

Conclusion

The next potential market-moving event will be the decision of the Fed on December 18 to reduce its benchmark interest rate by .25% or not.

While a reduction was widely expected only a month ago, it is now less certain. Rising long-term bond yields and an inflation rate that remains a bit above the Fed’s 2% target may lead it to postpone a further easing until February 2025.

That being said, December and January are months that are good to investors. With or without a Fed easing decision.

Let’s, therefore, enjoy it while it lasts.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980