Overview

In March, the S&P 500 lost 5.57% overall, while the Nasdaq composite slumped 8.14% and the Russell 2000 (Small Cap Stocks) cratered 6.81%.

Internationally, a weakening USD helped developed markets fare much better than their US counterparts. The EPAC BM Index of developed economies (ex-US) lost .95% and emerging markets did relatively well, the MSCI EM (emerging markets) rising .38% and the MSCI Frontier 100 index a greater 2.97%.

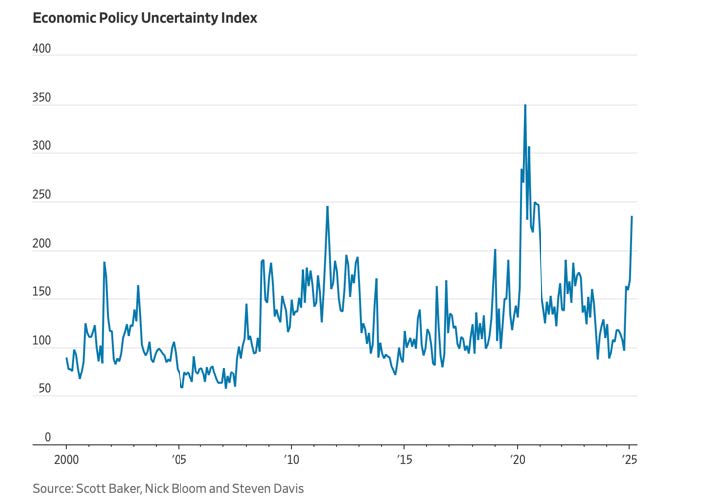

Political uncertainties are mostly to blame this past month for the dismal US equity market performances, as illustrated by the chart below:

The sharp rise in economic uncertainty associated with the long-term effects of the Trump Administration’s posture regarding tariffs, the economic retaliation that will ensue, as well as their impact on consumption and growth overall, led investors to withdraw from US equities in favor of international ones, gold and, to a lesser degree, US bonds.

In this highly uncertain environment, US fixed income markets held up generally well. The AGG index finished the month with a tiny .04% gain, while Investment Grade and High Yield bonds suffered modest losses, respectively .29% and 1.02%. The Bloomberg municipal index was down 1.69%, in good part due to seasonality.

Our median portfolio was down 1.78% in March. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) lost 1.85%. Year to Date (YTD), our median portfolio is up .98% vs. .90% for our benchmark.

Market developments

Signs of economic weakening are starting to worry US investors and economic observers. While indicators of this deteriorating economic backdrop remain mostly concentrated on “soft data” indicators, such as the one below, more professionals feel that it is only a matter of time until “hard data”, in the form of lower GDP growth or higher unemployment levels, for example, catches up to the “soft data”.

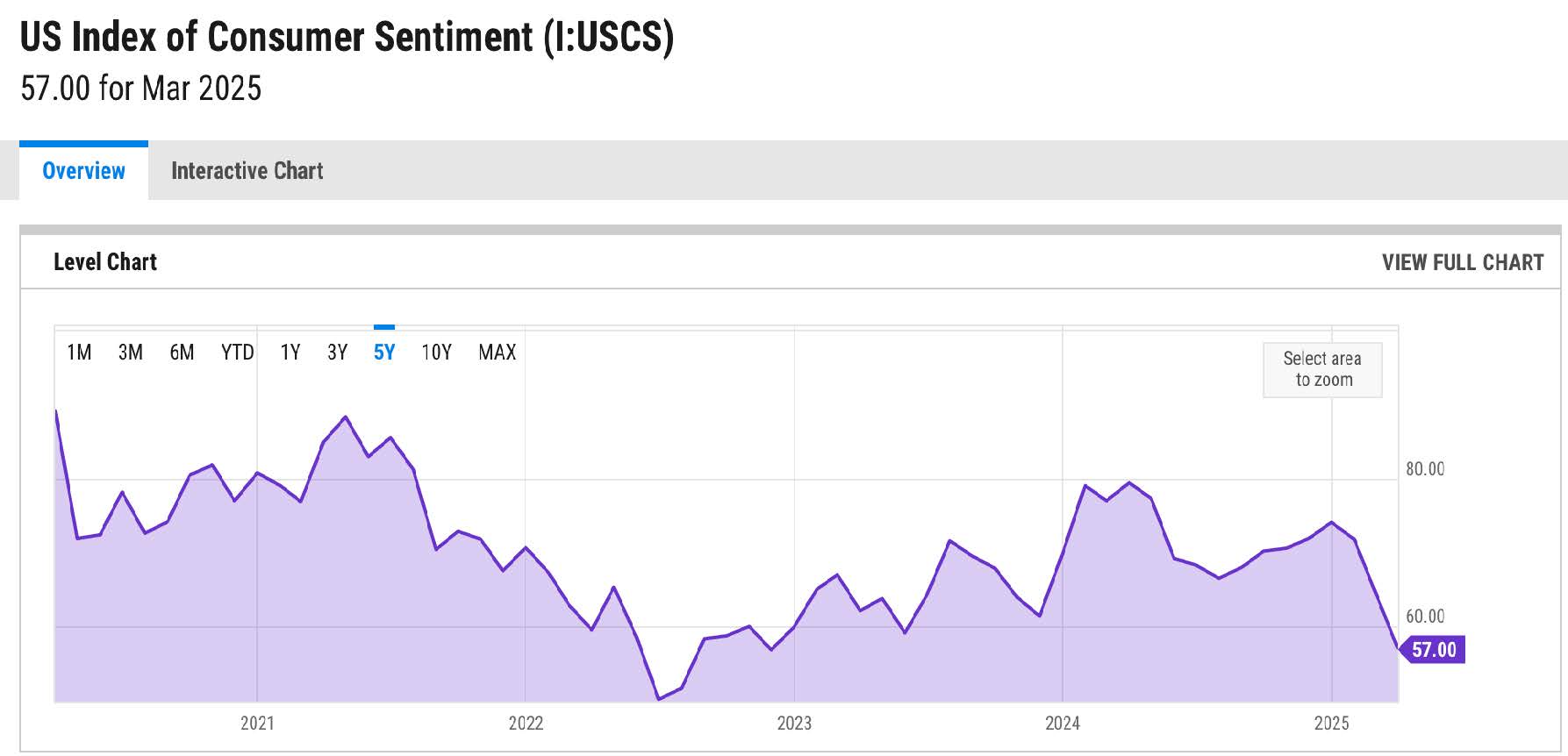

For now, consumer confidence seems to be the most troubling part of the economic puzzle, as shown below:

The sharp decline in consumer confidence since the beginning of 2025 appears to be the response of the US consumer to the initiatives, economic and political, of the new US Administration. The American consumer appears to be skeptical of their long-term economic effects and prefers to maintain a cautious “wait and see” attitude. With consumption accounting for two-thirds of the US economy, the implications could be serious.

As a matter of fact, the word “recession” is re-entering the economic literature after a bit of an absence. The probability of an economic recession is still low, estimated at 25% as of a few days ago in a Schwab Market Overview Webinar I attended. Their market strategists estimate that the economy will slow over the coming months, possibly going into a recession. In their view, this could lead the FED to cut interest rates in response, twice before year-end.

However, the Fed’s actions are only likely to take place after unemployment has risen. The release of the unemployment report for March at the end of this week will provide more clarity on this point.

Portfolio Commentary

In March, early in the month, I continued to de-risk our portfolios. After reducing our tech exposure (sale of QQQ) in favor of AGG, on February 25, I sold SPY in favor of IEFA, the International Developed Market ETF. This last move did not reduce our equity allocation overall but rather diminished partially our US equity allocation in favor of non-US equities. Due to high US equity valuations and political instability, I felt a reallocation, even if moderate, was justified.

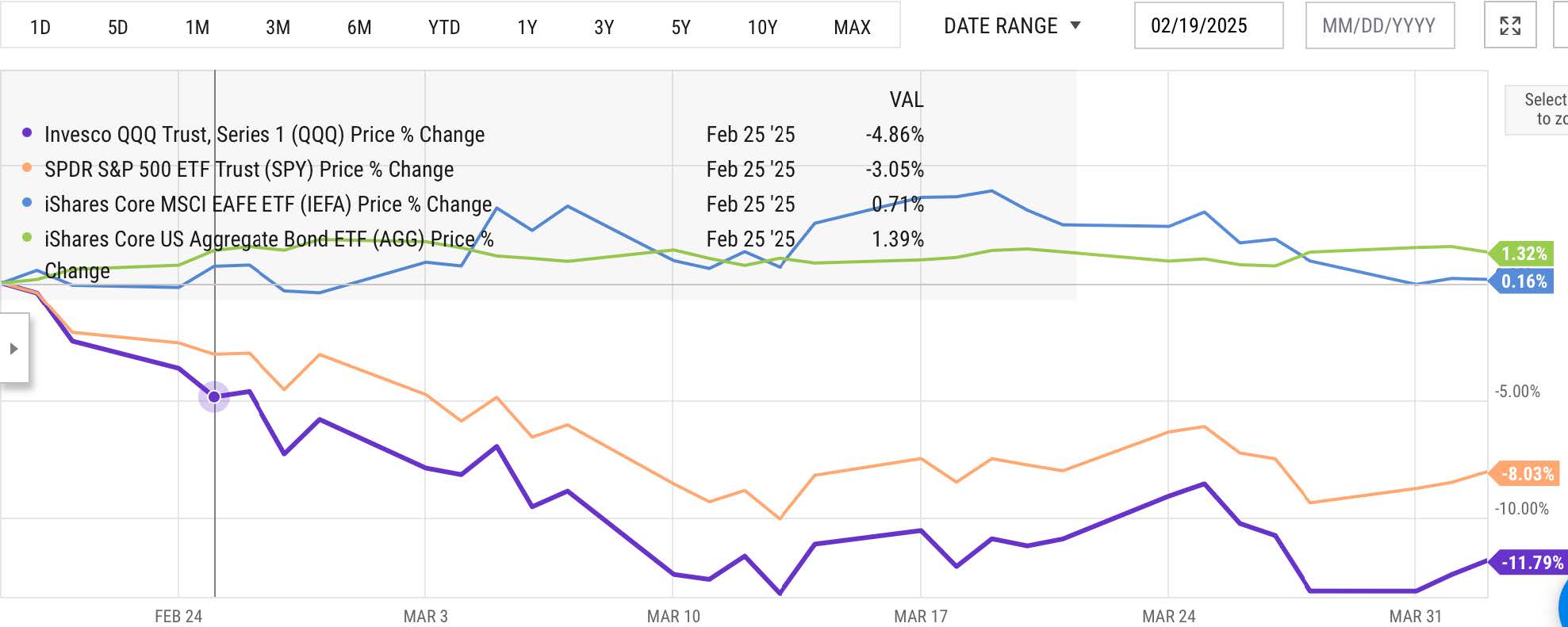

The chart below encapsulates our de-risking moves since February 25 (vertical line in the graph):

First, we sold a good chunk of our investments in QQQ (purple line) in favor of AGG (green line). Then, on March 5, we reduced our investments in SPY (orange line) in favor of IEFA (blue line). Both actions have allowed us to mitigate the effects of the downdraft in US equities that qualified, as of yesterday, as a correction (down 10% or more from top to bottom).

Looking ahead, I believe that the chance of a recession in the US has risen significantly due to the uncertainties created by the policies and the “out-of-the-norm” behaviors of the Trump Administration.

Until recently, many market observers thought that this new Trump Administration was open to adjusting and moderating their politics and related announcements, should markets turn negative. As of now, many believe that this Trump 02 version is more ideologically driven than the first.

In the famous words of Hannah Arendt: “to the ideologically driven mind, facts do not matter…”. With that in mind, it is possible that harsher economic and political punishment will be inflicted on all of us before Trump 02 changes its course.

Conclusion

We are living in unprecedented times. That is, unless we go back to the 1930s.

Managing emotions and portfolios has become particularly challenging. Teasing out what really matters from what does not from the constant noise emanating from the White House, both economically and politically, is quite a daily battle.

It happens rarely over time, but I believe that we are now at a point in our history where our politics have a real and direct impact on economic and market conditions. Specifically, I believe that based on the continued challenge to the Rule of Law that the current administration represents, economic and market uncertainties are bound to remain or increase. How could it be otherwise if the referee (US government) decides what the rules of the game are as the game is being played and applies them at it sees fit.

I have been applying a defensive strategy to the management of your portfolios since inauguration time. It has served us well so far. Based on my current assessment of market conditions, I plan to continue to do so for the foreseeable future.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980