Overview

Equities performed nicely in January after several ups and downs due in part to the often unpredictable and sometimes almost incoherent nature of many of the policy decisions made or announced by the new US Administration. Nevertheless, good overall economic data prevailed in the end, as illustrated in our first graph below.

The S&Ps’ 500 rose 2.78% overall while the Nasdaq composite gained a lesser 1.66% and the Russell 2000 (Small Cap Stocks) increased with a 2.62% monthly performance.

Internationally, the EPAC BM Index of developed economies (ex-US) gained 4.90%. Emerging markets fared relatively well, the MSCI EM (emerging markets) rose 1.81% and the MSCI Frontier 100 index a lesser .76%.

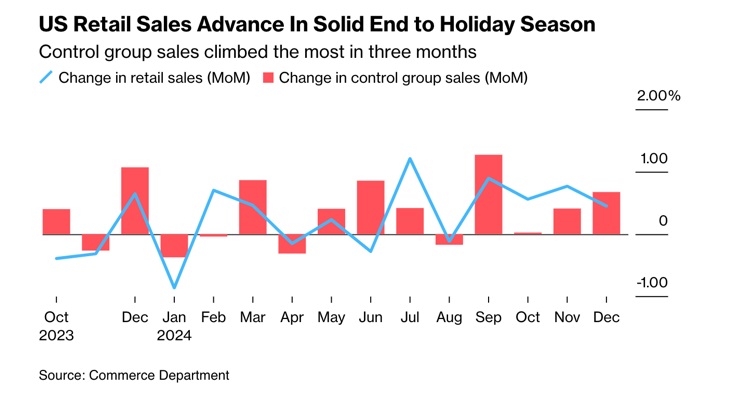

The chart below illustrates the resilience of the US consumer throughout the past year and particularly during the crucial year-end period. Together with relatively tepid monthly inflation numbers, both sets of data were encouraging and helped push equities forward.

In January, US fixed-income markets performed relatively well. The AGG index finished the month with a .53% gain, while Investment Grade and High-Yield bonds rose respectively .55% and 1.37%. The Bloomberg municipal index was up .50%.

Our median portfolio was up 2.25% in January. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 1.83%.

Market developments

Market volatility remained high in January. The causes are largely known and were partially summarized in my December commentary:

“Uncertainty concerning the effects of anticipated US tariffs on the global and US economy, on inflation and on consumption; uncertainty concerning the chances of passage of the tax and regulatory agendas of the new administration; uncertainty and concerns about the changing geopolitical order have all contributed to the febrile market environment as 2024 waned”.

That sentiment has not subsided yet. That said, some policy moves by the new US Administration are starting to become clearer and their implications more discernable.

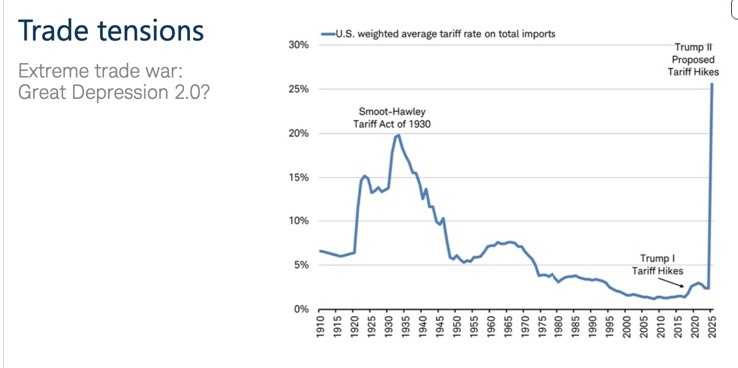

One area where economic uncertainty remains high, though, is that of tariffs. The chart below illustrates the potential effects of the Trump tariffs should they be enacted as announced.

In this highly uncertain environment, Investors need to remain patient and not overreact to any destabilizing piece of news. The reality so far is that, on the economic front at least, there is often a noticeable difference between what the new US Administration announces and what it does.

Portfolio Commentary

In January, I sold two-thirds of our SCHW investments after its shares it bounced up 11% on the back of solid quarterly earnings and prospects. We remain invested in SCHW. I anticipate another price jump in the coming weeks. We will exit this investment then.

Elsewhere, I continued to reduce our overall equity investments in a measured way selling from 3% to 5% of clients’ assets due to valuation concerns, as illustrated in the graph below:

The high valuations and particularly in the tech and growth sectors have continued to justify portfolio adjustments in favor of RSP (equal weight ETF) and VTV (Value ETF), as well as the outright sales of equities, as in the case of our SCHW investment.

Dollar for dollar, the moves away from equity ETFs that track capitalization indices (selling SPY) or that favor growth (selling QQQ) in favor of RSP and VTV, respectively, have contributed to reducing our overall risk level, while avoiding too sharp a reduction in our equity allocation.

The justification for this strategy was briefly vindicated by the end of January when the DeepSeek AI application caused a market swoon in the tech sector. While the market reaction was ephemeral this time around, with extreme valuations in that sector another such development combined to a geopolitical misstep, for example, could well have longer-lasting consequences. We will maintain our prudent positioning for the time being.

Conclusion

I think that it is fair to say that part of the remarkable economic success of the United States over the past two centuries, and particularly since the end of WWII, is attributable to its relatively stable political environment and to a fundamental respect for the Rule of Law within its jurisdiction.

From its release of insurrectionists charged for their actions on January 6, 2021, to its firing of FBI agents who oversaw the inquiries that led to those charges, to its use of DOGE as if it were an Agency of the government when it is not, to the outsized influence of unelected officials over policy or the cozying up with tech sector billionaires, respect for the Rule of Law and, as importantly, for the spirit of the law seems to be of no concern to the new administration.

I muse over how long it will take for those types of decisions to inflict pain on our economy, be it via greater inflationary pressures, rising unemployment or market corrections.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980