Overview

US and World equity indices were down in December, for the most part. An increasingly loud drumbeat of recession talk spooked investors.

The S&P’s 500 slumped 5.76%. The Nasdaq Composite collapsed 8.67%. Internationally, the situation was not as dire. The EPAC BM Index of developed economies stayed flat for the month thanks to a weakening USD (down 2.14% this past month). Emerging markets were slightly down (1.41% for the MSCI EM).

The US bond market was down too but less significantly. The long bond lost 1.70% (it has lost 29% in 2022). Elsewhere in the fixed income sector, the S&P’s Muni index slipped .12% and the high yield Bloomberg index .62%.

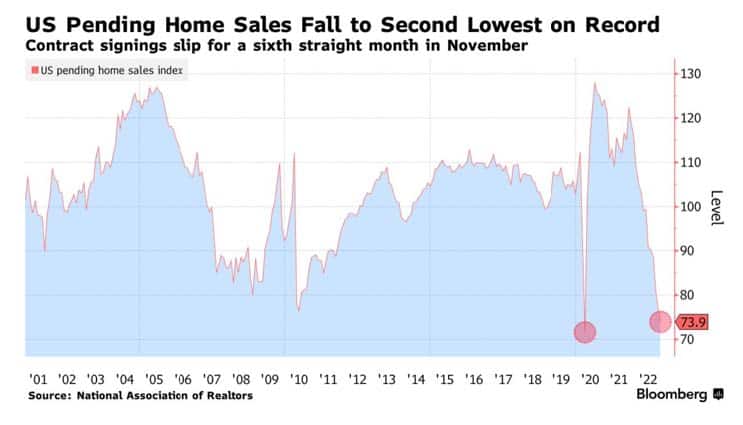

Below is a chart that illustrates the fear of economic recession that has consumed investors in December.

In November, pending home sales registered one of their worst performance on record, feeding the “recession narrative” that now has seemingly replaced the “inflation narrative” of prior months.

In December, our median portfolio lost 2.02%. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) slipped 2.75%. In 2022, our median portfolio lost 17.35% vs. 15.70% for our index.

This was a disappointing performance caused by small yet painful investments in single stocks, at the end of 2021 and in January 2022. Single stock investing is an approach that I rarely employ. I will eschew it even more going forward.

Market developments

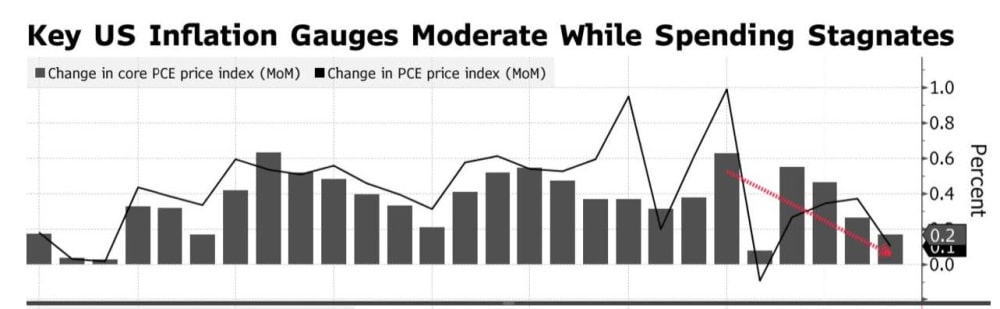

In December, the overall level of inflation in the US economy dropped, as illustrated in the table below:

The PCE index (Personal Consumption Expenditures), the favored inflation gauge of the Federal Reserve Bank (FED) , rose a mere .2% compared to .5% in October. This was a better number than what was expected. On a yearly basis, the PCE index is now at 6.02% vs. 6.27% earlier. This is undeniably good news.

Nevertheless, it was insufficient to prevent market participants from feeling that this gradual reduction of the level of inflation would not warrant a rapid loosening of monetary conditions. This was somewhat justified by the strong employment report that followed by a few days. That report showed continued strength in the job market with wages increasing 5.09% on a yearly basis vs. an increase of 4.92% in the prior month. Markets lost momentum as a result.

Better than expected CPI numbers, released in the middle of the month, did not change the tone of the market. The US CPI is now running at a 7.11% annual pace vs. 7.75% the prior month. This better-than-expected development caused equities to initially jump up 2% to 3%. However, the market improvement was not sustained as market analysts felt that the service component of the index remained stubbornly high.

Because the place held by services in the US economy is larger than that of manufactured goods or raw materials, a drop in product inflation is less impactful than a drop in say “hotel or transportation” prices for example. This is what happened with the most recent inflation numbers. Energy prices dropped substantially but service prices did not drop as much. Investors would have liked to see the reverse and showed their disappointment by selling equities.

Tilts and Allocations

In December our allocations remained unchanged.

Good relative performances from our Air Liquide and IAU (gold) holdings as well as from our other non-US investments, helped us reduce the damage caused by unrelenting selling pressures throughout the month.

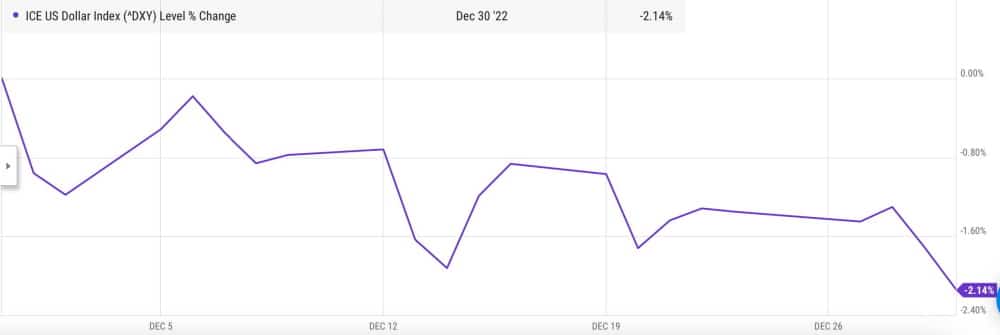

The quasi-continuous loss of value of the USD, shown below, explains in part our outperformance in December.

The USD lost a little over 2% in December against a basket of its major trading counterparts. It nevertheless gained a little over 8% in 2022.

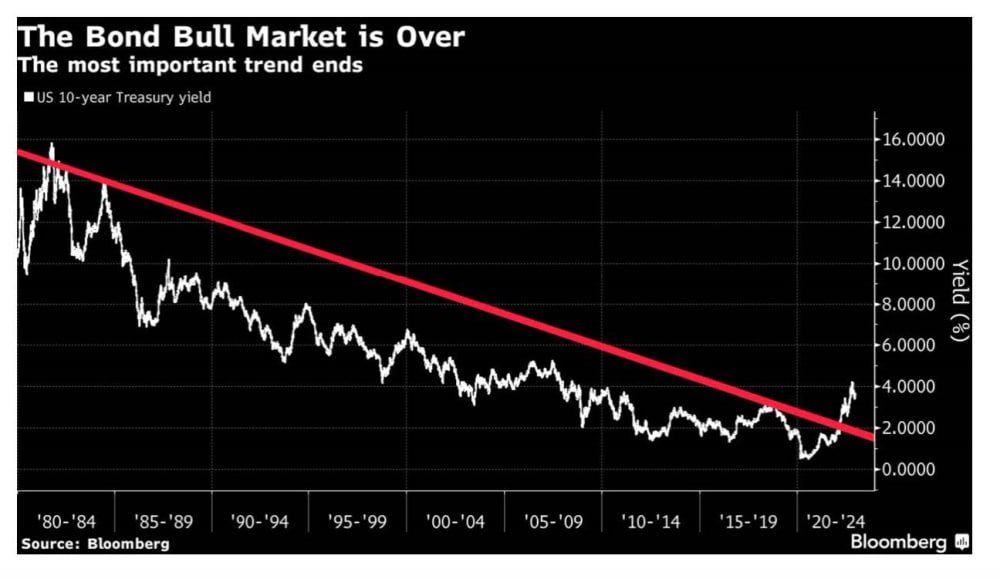

I would like to conclude this newsletter with the striking chart below:

It depicts the yield on the 10-year US treasury since 1980 and shows how the current FED policy has broken the long-term trend of interest rates. We may be entering a new era where valuations matter more and where financial excesses are punished rapidly. The tech sector appears particularly vulnerable in this context.

Conclusion

How long will the FED policy that caused the recent spike in interest rates illustrated above last is anyone’s guess. The answer to this question though is key for equity investors in 2023. The timing of that change (“pivot” in current parlance) will affect the performance of equities this year.

For now, as I indicated in my previous newsletter, the risk of recession is increasing and that automatically will lead to lower corporate earnings, the main engine of equity performance. The difficulty that investors face is to accurately weigh the odds of lower corporate earnings in the next two or three quarters against the positive news associated with lower inflation and of a more accommodative monetary policy.

As 2023 unfurls, I have not yet seen anything to make me think differently. The next few months are likely to be quite volatile.

Please feel free to reach out to me with any questions.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980