Overview

Equity markets ended the year with a thud, partially the consequence of a more hawkish message from the Federal Reserve Bank (FED), around the middle of the month.

The S&P’s 500 dropped 2.38% overall while the Nasdaq composite lost only .55% and the Russell 2000 (Small Cap Stocks) cratered with a whopping 8.26% monthly loss.

Internationally, losses were generally similar to those in the US. The EPAC BM Index of developed economies (ex-US) dropped 2.51%. Emerging markets fared better, the MSCI EM (emerging markets) dropped only .29%, thanks to oil prices firming up a bit.

The USD continued to gain against most currencies, aided by the hawkish tone from the FED and by the continued threat of tariffs likely to be imposed by the incoming US Administration.

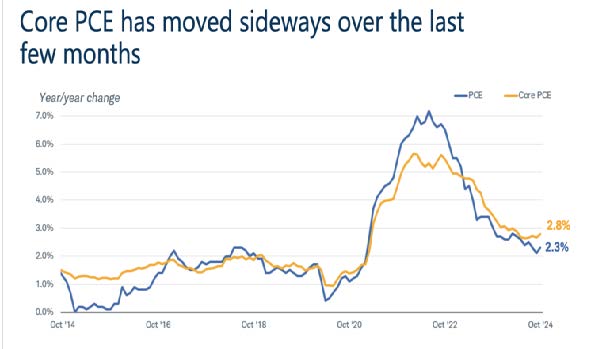

The chart below is yet another illustration of how complicated the FED’s task is: specifically, how to reduce interest rates to allow the economy to grow but not so that it will reignite inflation, which could come from accelerating consumption. In spite of elevated mortgage rates, home sales seem to be picking up, further confirming the health of the US economy. That, in turn, does not imbue the FED with a sense of urgency to further relax monetary policy. Equity investors wish it were otherwise.

In December, US fixed income markets performed poorly, as could be expected from a less accommodative monetary policy. The AGG index finished the month with a 1.64% loss, while Investment Grade and High Yield bonds lost respectively 1.94% and .43%. The Bloomberg municipal index was down 1.46%.

Our median portfolio was down 2.75% in December. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) lost 2.17%. In 2024, our median portfolio, net of fees, was up 10.25% vs 9.39% for our reference index.

Market developments

An economy that performs well, such as the US economy, should be a cause for unmitigated satisfaction. However, the fine line between “performing well” and “performing so well that the FED will slow or stop its interest reduction cycle” seems to be a hard one to hold.

Equity investors have been moving from euphoria in November to concerns in December as the economy continued to show signs of good health and the FED hardened its message on the back of “sticky” inflation numbers, as shown below:

Market volatility increased significantly in December.

Uncertainty concerning the effects of anticipated US tariffs on the global and US economy, on inflation, and on consumption; uncertainty concerning the chances of passage of the tax and regulatory agendas of the new administration; uncertainty and concerns about the changing geopolitical order have all contributed to the febrile market environment as 2024 waned.

Nevertheless, 2024 has been a resounding success for US equity investors. While fixed-income portfolios made a negligible contribution to performance, the stellar one offered by the large-cap sector, in particular, more than compensated.

The S&Ps’ 500 and the Nasdaq finish the year respectively with annual performances of 25.1% and 29.6%.

Portfolio Commentary

In an environment of increasing volatility caused by economic, regulatory, tax and geopolitical uncertainties, I refrained from any activity this month, other than “cash recycling” (buying new US T Bills with the proceeds from expiring ones).

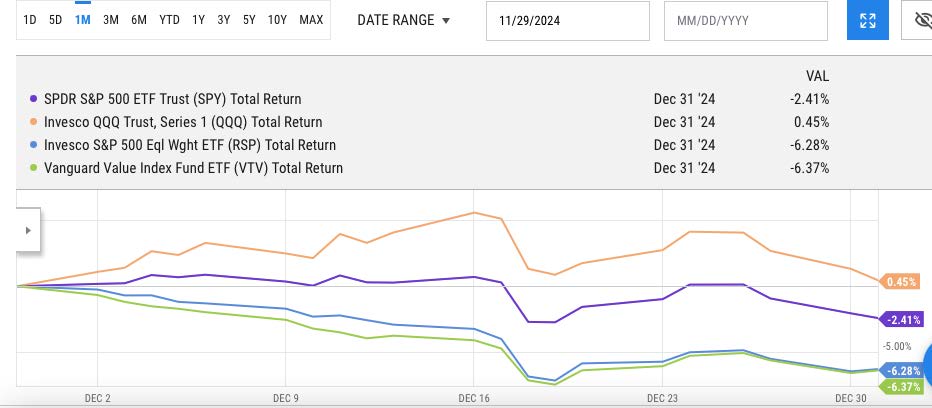

Lack of visibility led investors to move back into tech/growth equities in a forceful way, at the expense of all other sectors. The chart below illustrates this reality:

The dichotomy in performances between the tech/growth sector of the US equity markets (orange line) and rest of the market (blue and green lines) was striking in December. This sharp divergence explains our underperformance this past month. With an eye on overvaluation, I have gradually moved our portfolios away from tech (relatively speaking) and into VTV (value) and RSP (equal weighing). This has cost us in December.

Reflective of this situation, our now small investment in SCHW suffered a 10% loss this past month. Meanwhile, the USD went up another 2.5% causing international equities to stall. Air Liquide was flat this month. The USD was up 7% in 2024, against a basket of major currencies.

Overall, we finish the year slightly ahead of our benchmark with annual portfolio performances ranging from 7.6% to 19.84%, with our median portfolio ending up with a 10.25% performance.

Conclusion

2025 will bring about its set of surprises. No doubt, political, economic and regulatory decisions will alter our short-term views of market direction.

For now, US markets are expected to continue to perform reasonably well, supported by massive corporate investments in artificial intelligence applications. Should this expectation be realized, still higher valuations in the tech sector will become harder to justify and to sustain. As the year progresses, the chance of a speculative bubble bursting will increase. I will try to stay ahead of this.

Thank you for your continued trust and Happy New Year to all!

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980