Overview

In June, the S&P’s 500 rose 3.59% while the Nasdaq Composite jumped 6.03%. The Russell 2000 (Small Cap Stocks) declined .66%. In international markets, the EPAC BM Index of developed economies (ex-US) dropped 1.58%. The MSCI EM (emerging markets) progressed a strong 4.01%.

These bifurcated performances result from the continuing good health of the US economy, juxtaposed to a deteriorating political situation in Europe, where recent elections brought extreme right politicians on the cusp of power. The potential negative implications due to more permissive budgetary policies caused bond markets in Europe to drop and bring equities down in their wake, in France in particular.

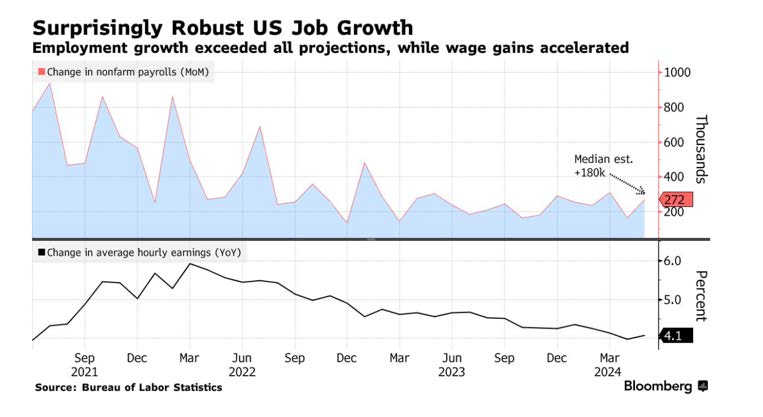

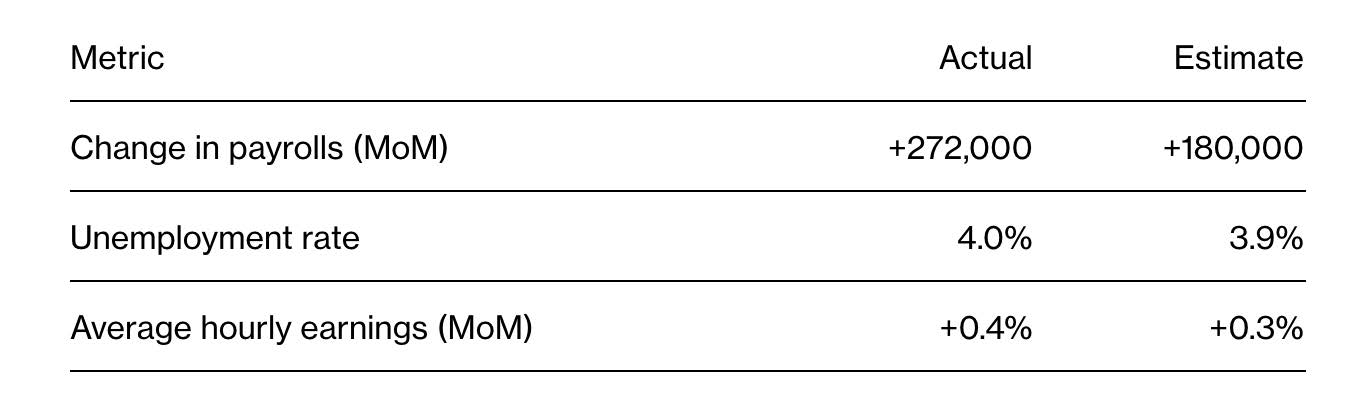

Stateside, so far good economic data was still driving market behavior in June. The unemployment picture, illustrated below, offered a case in point:

US fixed income markets performances were positive in June. The AGG index was up .95%, while Investment Grade and High Yield corporate bonds rose respectively .64% and .94%. The Bloomberg municipal index was up more significantly at 1.53%.

In June, our median portfolio gained 1.14%. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 1.46%. YTD our median portfolio, net of fees, is up 6.17% vs 5.33% for our reference index.

Market developments

Positive economic data continued to undergird the performance of US equities in June. A surprisingly strong employment market, as indicated in the metrics below,

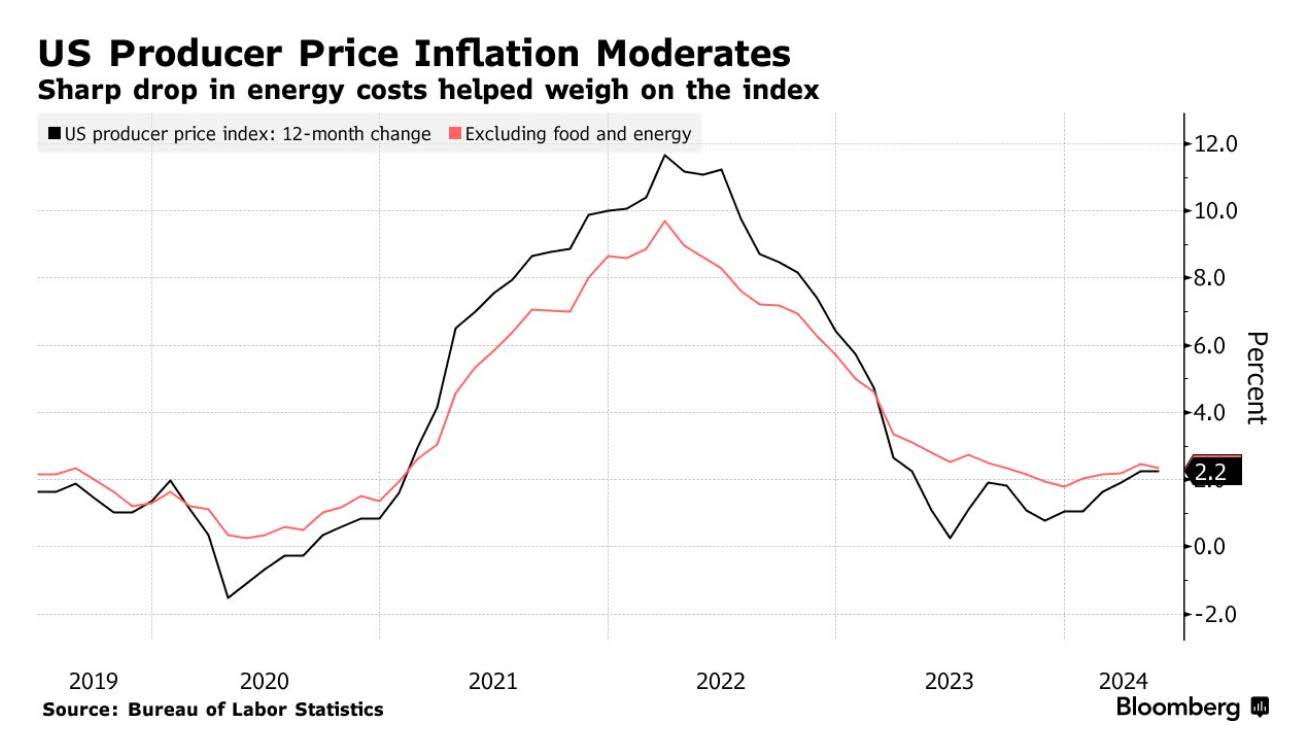

coupled with improvements on inflation propelled equites up.

Internationally. poor election results from mainstream parties in the European Parliamentary elections caused bond markets there to drop (yields up), particularly in the case of France. We will know next month what the impact could be, on a long-term basis.

In France, if Lepen’s party, previously known for antisemitism among other unpalatable features, obtains a majority of seats in the National Assembly, budget deficits could increase significantly.

This is what caused bond yields to rise there and equity markets to drop meaningfully allover continental Europe in June.

Portfolio Commentary

During the month of June, I reduced by about 33% our investments in international equities.

Two concerns motivated this reduction in our risk posture: 1) Our entering a period of the year that typically retracts from performance, 2) Increasing concerns about political extremism in key corners of the world (Europe and the US) and their economic repercussions.

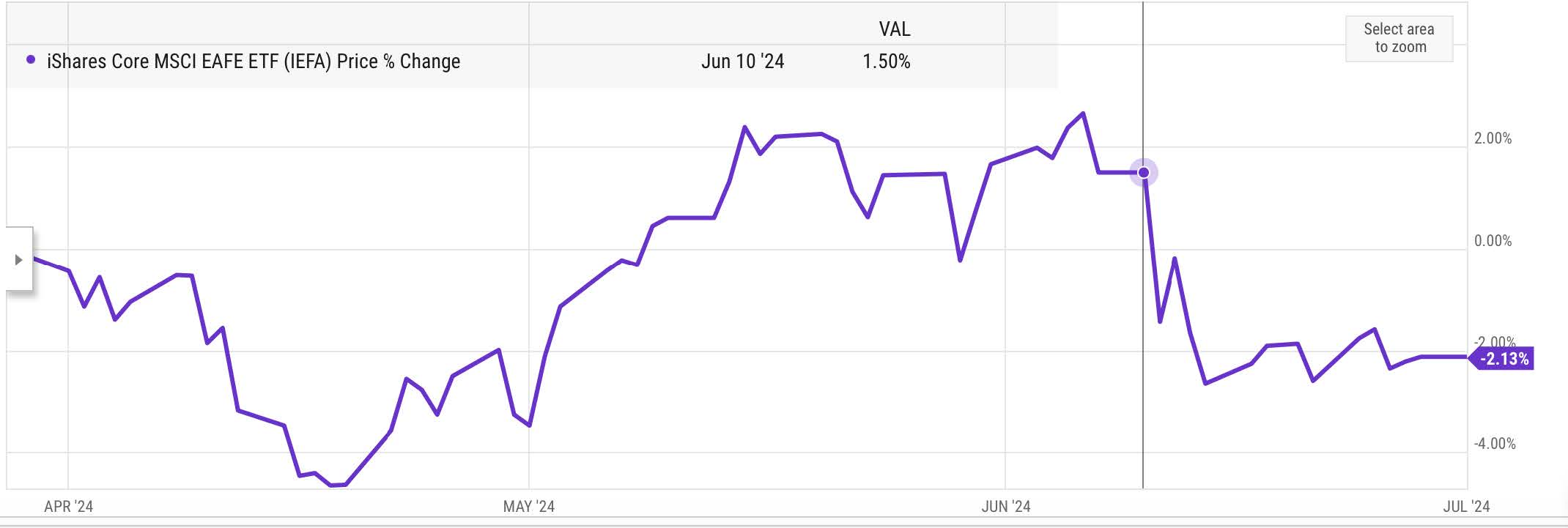

I sold IEFA, the international developed markets ETF, in order to reduce our overall exposure to non-US equities as well as to deflate a bit our allocation to equities in general. As a result, our allocation to equities has dropped by about 3% to 4% across most portfolios.

Below is a chart of IEFA’s performance in June. The vertical line marks the day when President Macron of France called for snap parliamentary elections there, in my view, to wrong-foot his opposition in the French Parliament. We will know in ten days whether that was a good political calculation or a disastrous one.

Over the past few days, Lepen’s party has toned down its budgetcrushing rhetoric and equity markets were up sharply in France today as a consequence. Bond yields have dropped a bit and our own Air Liquide bounced up nicely.

Meanwhile, it the US the exact reverse seems to be happening. Bond yields have risen sharply over the past two days as investors digest the disastrous performance of President Biden, this past Thursday, and the implications for economic policy going forward.

A Trump victory in November could bring about higher inflation and larger budget deficits, or so seem to think bond investors.

Conclusion

The current political environment, here and in Europe, is fraught with risks that compound the difficulty of navigating markets and managing portfolios.

Over the coming weeks, I will remain particularly focused and attentive to news, economic and otherwise, that could have an impact on medium and long-term market performances. I may adjust portfolios abruptly and significantly as a result.

Thank you for your continued trust and Happy Fourth!

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980