Overview

In May, equity and bond markets bounced back from their dismal April performances in the US and globally.

The S&P’s 500 rose 4.96% while the Nasdaq Composite jumped 6.98%. The Russell 2000 (Small Cap Stocks) increased 5.02%. In international markets, the EPAC BM Index of developed economies (ex-US) gained 3.06%. The MSCI EM (emerging markets) progressed a meager .29%.

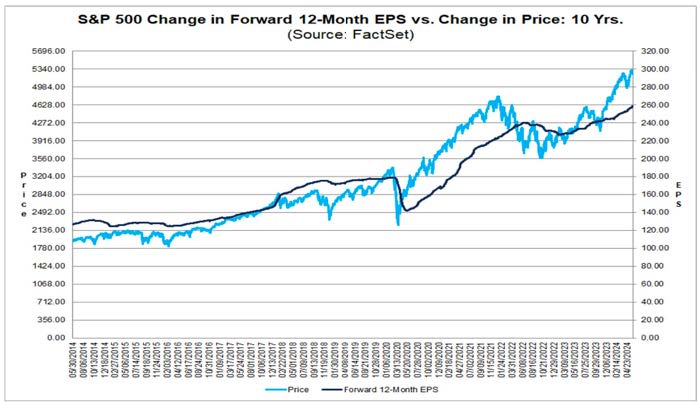

Good corporate earnings for the first quarter of 2024 continued to support equities in the US. As of May 31, and with 98% of S&P’s 500 firms having reported, 78% had earnings that beat estimates. In addition, earnings progressed, year-over-year, by 5.9%, after flattening for most of 2023, as shown in the graph below:

The dark blue line illustrates the progression of corporate earnings over the past ten years. Notice how it slopes upward on the right side, after a rather flat period for most of 2022 and 2023.

Fixed income markets bounced back in unison with equities in May. The AGG index was up 1.70%, while Investment Grade and High Yield corporate bonds rose respectively 1.80% and 1.10%. The Bloomberg municipal index was down a bit at -.29%.

In May, our median portfolio gained 3.11%. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) rose 3.13%. YTD our median portfolio, net of fees, is up 5.16% vs 3.79% for our reference index.

Market developments

In May, in addition to supportive corporate earnings for the first quarter of 2024, equities benefitted from economic data releases that calmed markets down.

First, the unemployment number for April, released at the beginning of the month, showed continued moderation in its wage growth component. Specifically, US average hourly earnings progressed only .20% in April. That brought the annual wage progression to 3.92% vs. 4.11% the prior month, as shown below:

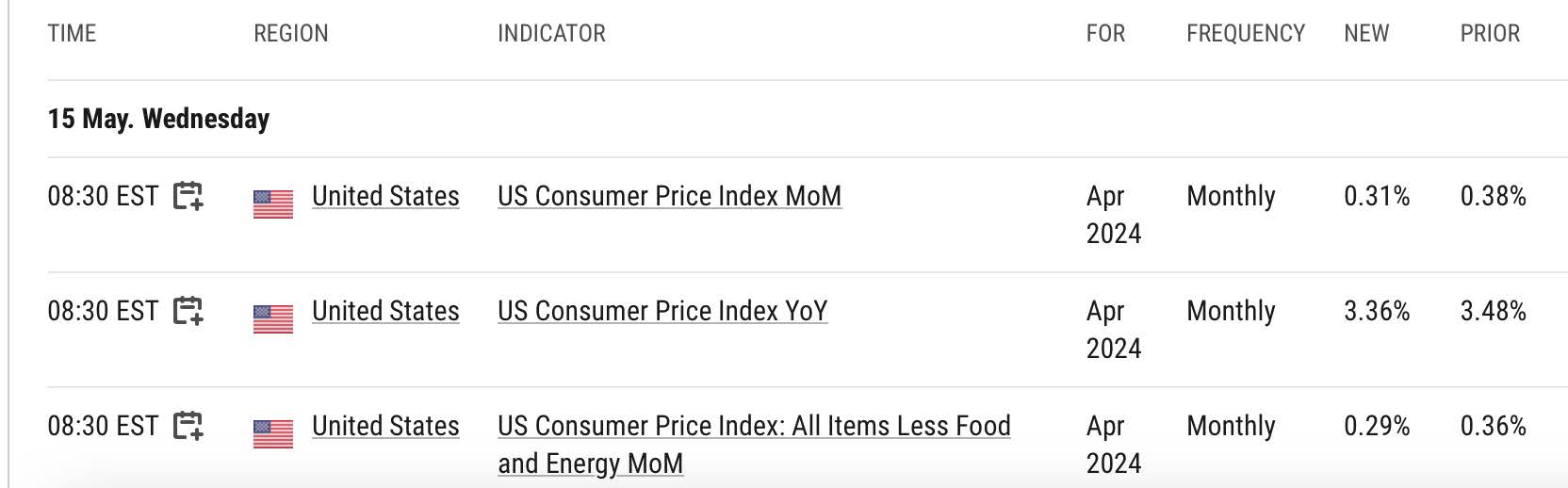

Then, at the mid-point for the month, inflation numbers for April, came in relatively low, counteracting the spike of the prior three months, as shown below:

Both sets of numbers continued to support the narrative of a moderating inflation combined to a resilient job market.

Looking ahead a bit, all we need now to further sustain the equity gains of the year, is continued moderation in inflation and the avoidance of a serious economic slowdown. However, there are signs of slower manufacturing activity overall. Should that be followed by a slowdown in the service sector, we might be facing difficult summer months.

Portfolio Commentary

Our two idiosyncratic stock investments underperformed in May.

Specifically, SCHW went down .58% overall, after going up and down more that 10% in the space of three weeks. The volatility of the stock price seems to have to do with their underwhelming 2nd quarter earnings projections and the hesitant commentary given by their new Chief Financial Officer who delivered the news to stock analysts. After approaching $80/share prior to this exercise in communication, the stock retreating to $70 (it is now around $72). After reading excerpts from this interaction, I do not see much to be alarmed

about. Public speaking can be difficult, particularly when facing equity analysts, brainy and skeptical individuals for the most part.

Air liquide went up only 1.24% in May and underperformed on a relative basis. There is no particular reason for this underperformance other than large market flows, in and out of the stock, around the payment of its annual dividend. Volatility should subside going forward.

Our other (non-stock) idiosyncratic investment is with GBTC, the Bitcoin ETF. It progressed 15% in May, erasing in the process its losses of the prior month. GBTC is up 75% year-to-date.

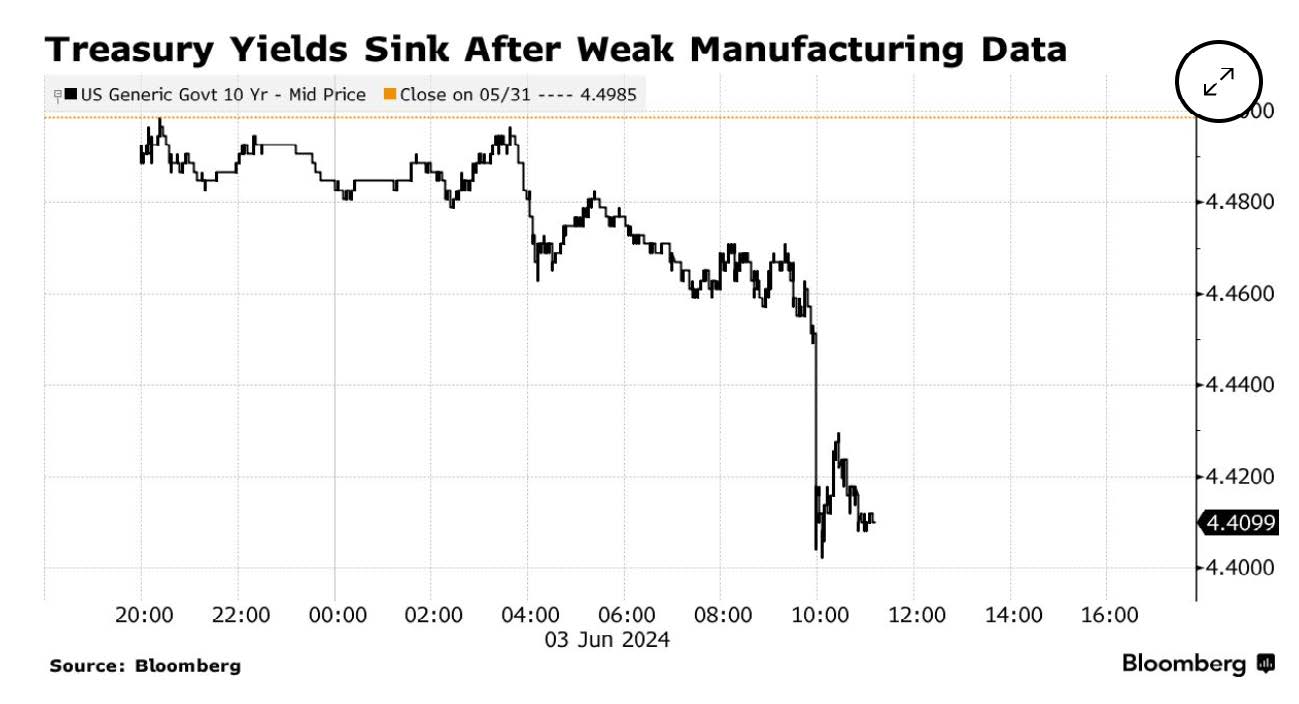

Overall, I have not altered our allocations. I am in a “wait and see” mood. Lower bond yields brought about by weak economic data, as shown below, could justify a lower equity allocation.

However, I am not yet convinced that the sporadic economic weakness that has materialized here and there warrants it just yet.

Conclusion

With Summer fast approaching, equity investors should ready themselves for a few months of flat to negative performances. This is not a certainty, just a statistical reality.

In addition to seasonal factors, continued warring in the Middle East and Eastern Europe and on-going military provocations in the Sea of China, add a negative geopolitical dimension to the investment environment that makes it harder to assess and adjust for.

The volatility of the US political situation compounds this situation with yet another level of complexity.

All this to say that geopolitical, political and economic realities combined with seasonal factors make the current environment a particularly combustible one. Over the coming months, investment decisions will have to take this unusually high level of complexity into consideration. This

could lead me to abruptly reduce the risk profile of all portfolios.

Thank you for your continued trust!

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980