Overview

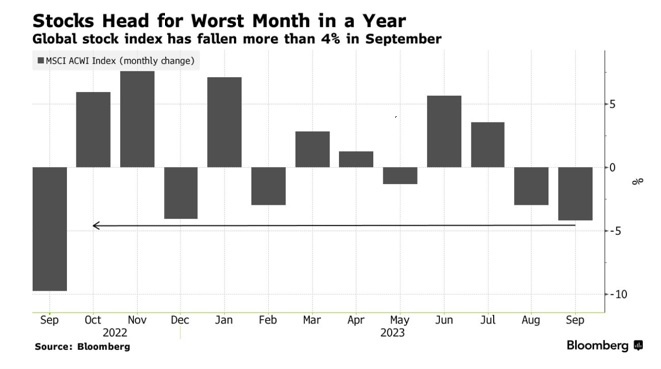

Statistically speaking, September tends to be a negative month for equity investors. The 2023 vintage fitted the pattern.

The S&P’s 500 lost 4.77%. The Nasdaq Composite declined 5.77%. Finally, the Russell 2000 (Small Cap Stocks.) dropped 5.01%. In international markets, the EPAC BM Index of developed economies (ex-US) declined 3.89% and the MSCI EM (Emerging markets) lost 2.81%.

If there is one reason that can explain this general deterioration in market sentiment it is the sense that higher interest rates may be with us for longer than previously thought. The “higher for longer” mentality is settling in and with it, the realization that perhaps the value of all types of assets, from bonds, stocks to real estate, is excessive and must go down.

The graph below testifies to that state of affairs:

In the fixed income sector, things got ugly as US bond yields rose sharply. Bond portfolios lost value. The US bond aggregate index dropped 2.54%. Corporate bonds declined 2.67% and the US long bond declined a very painful 7.30%. September was a repeat of the worst of 2022.

In September, our median portfolio declined 3.45%. Over the same period, a portfolio consisting of 50% ACWI (All Country World Index) and 50% AGG (US Bond Aggregate) lost 3.43%. YTD, our median account is up 4.12% vs. 4.46% for our reference index.

Market developments

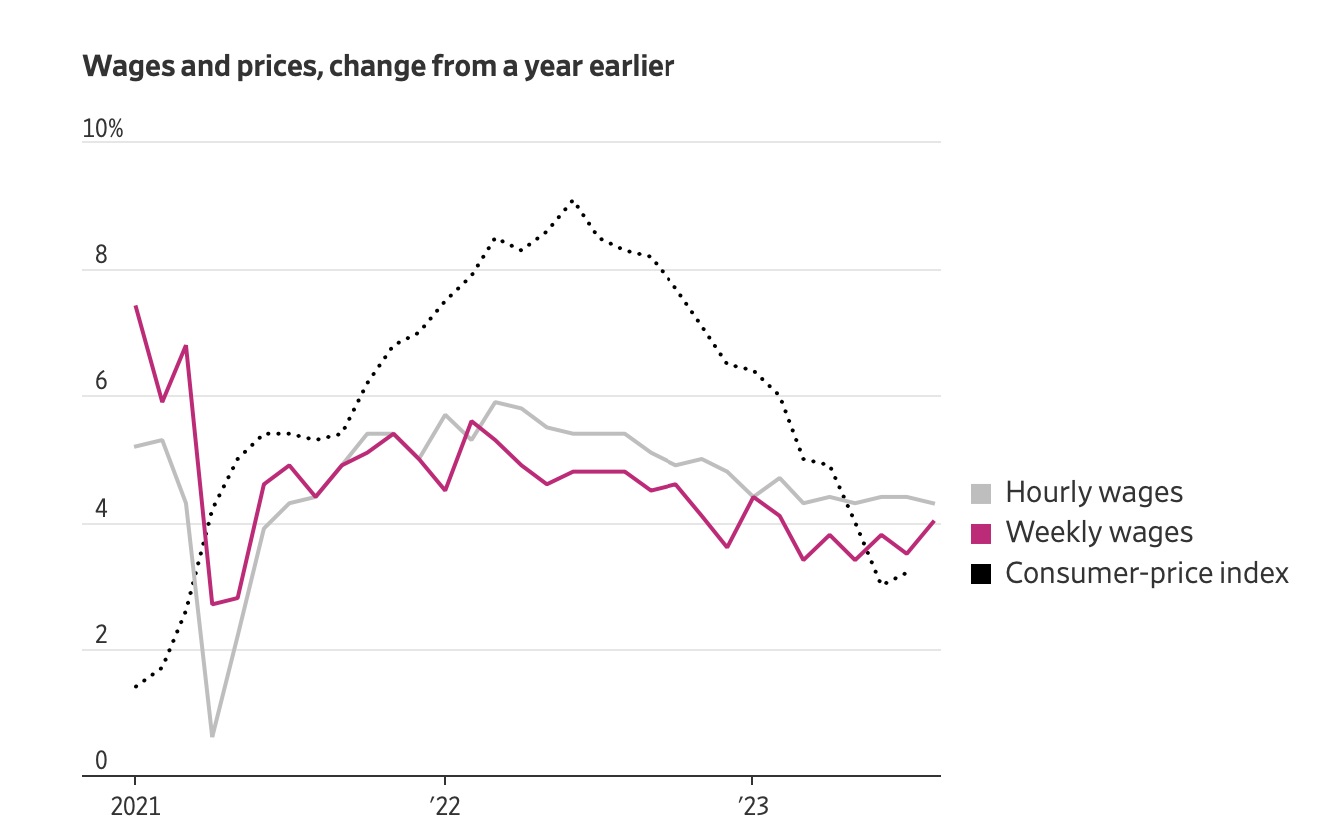

Economic news in September was relatively benign overall. Inflation continued on its downward trajectory, as shown in the graph below:

While wages increased a bit, all other data point to the continued downward trend in inflation, particularly with the US Core CPI dropping to an annual rate of 4.40% at the end of August vs. 4.70% the previous month.

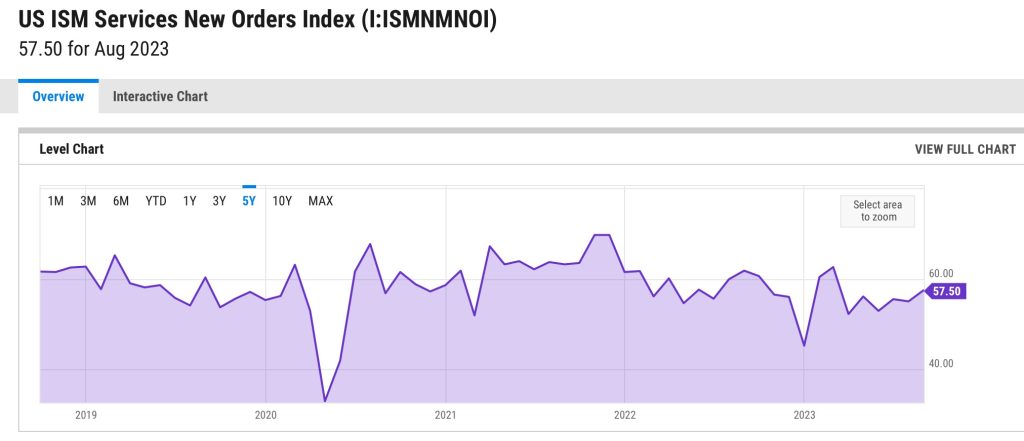

“Unfortunately,” the US economy remains relatively strong. The Institute of Supply Manager (ISM)’s latest release indicated that service orders, for example, were stable or increasing. A sign that the economy is not slowing much. See below:

This, in turn, tends to support the thesis that the Federal Reserve (FED) is not likely to reverse itself anytime soon. Hence the general market malaise.

Portfolio Commentary

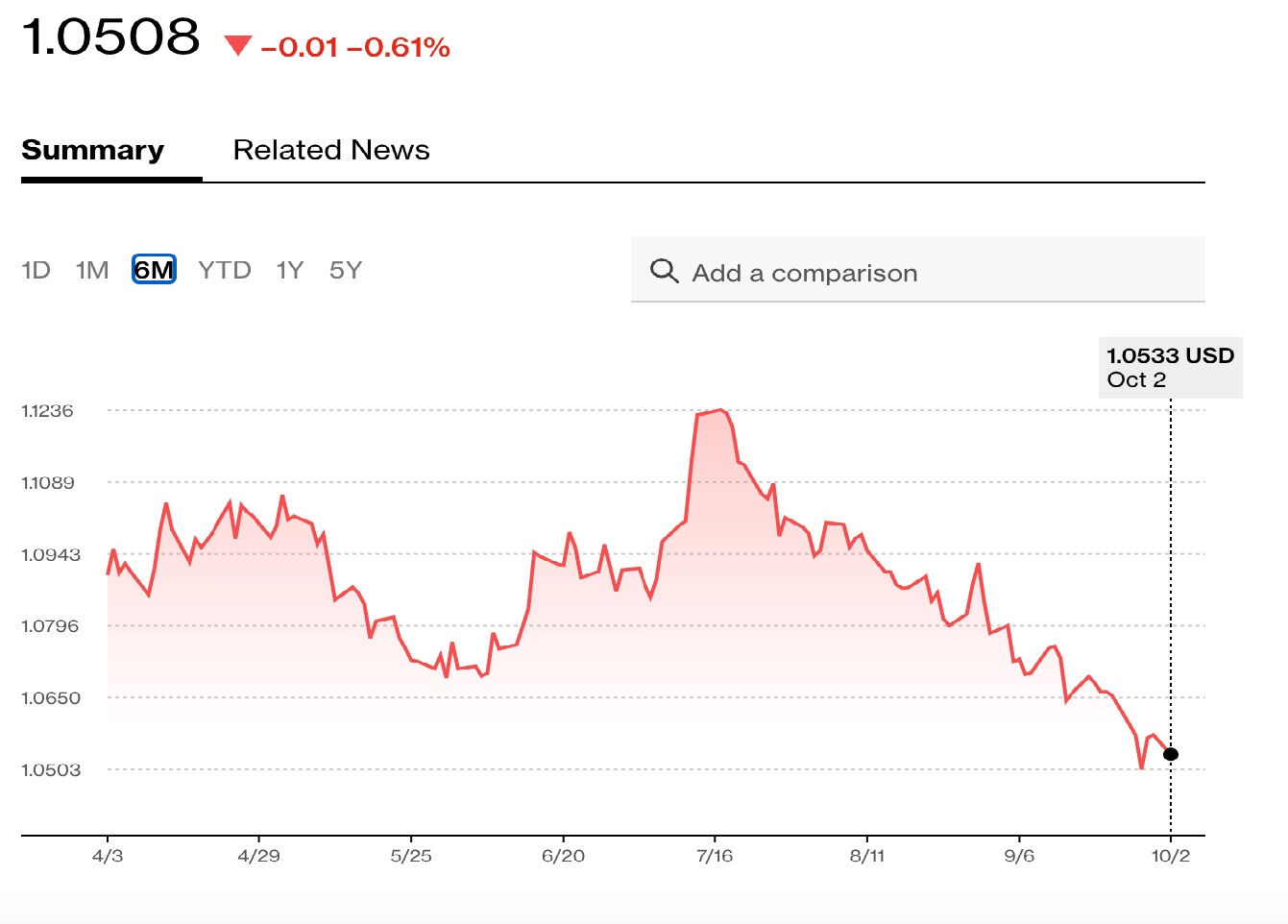

September was a difficult month. Our single stock holdings did not do well. SCHW (Charles Schwab) and AIQUF (Air Liquide) both lost about 7% during the month. In the case of AIQUF, a good 2.5% of the loss was due to the deteriorating exchange rate, favoring the USD versus the €. The € has been losing value for the past three months, at an accelerating pace it seems.

The graph below shows the decline from mid-July when it stood at 1.123 USD/€ to the current level of 1. 051 USD/€. That is a decline of 6.5%, over the past three months.

Often the increasing value of the USD is associated with its “haven” status. When the economic environment is not propitious or viewed as unstable, the USD will rise in value vs. other currencies, all things equal otherwise. However, in the current environment the USD rise is more likely the result of higher interest rates that make US government bonds more attractive than other government bonds.

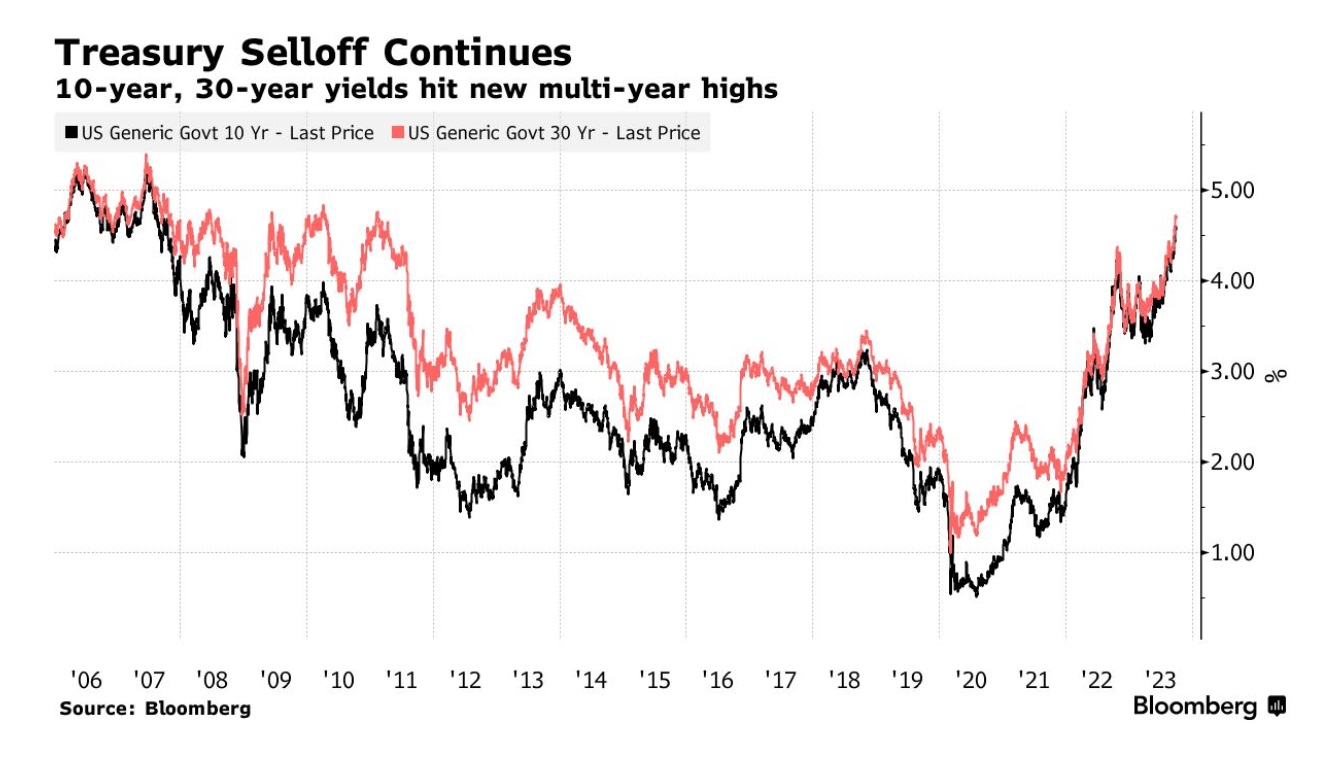

The graph below shows the impressive increase in yields of the 10 and 30-year US government bonds since the end of 2020:

Conclusion

We just averted a government shutdown. Interest rates could go higher and remain there for longer. UAW workers are striking. In general, Labor’s claims on a larger share of the economic pie are multiplying. All those factors add to the proverbial “wall of worry” that investors must climb.

The first day of October shows a lot of red. It’s been a bloodbath in the bond market, again, and stocks are declining. If it were not for the beautiful blue sky outside my office today, I would be abjectly down.

That said, I know that when it comes to investing, it is often when the situation looks particularly unpleasant that things turn around. And, since I started this newsletter with a reference to statistics, let me conclude with another statistical truth: the last quarter of the calendar year is, more often than not, a positive one for investors.

Thank you for your continued trust.

Jeff de Valdivia, CFA, CFP

Fleurus Investment Advisory, LLC

www.fleurus-ia.com

(203) 919-4980